By Ryan Ovenden, Wealth Advisor

Has the stock market ever caused you to feel anxious, or even fearful?

If you have investments and access to the internet, chances are the answer is yes.

Too often, we turn toward products in search of a safe place for our money during volatile times, but you’ll find that there aren’t any financial products that are 100% guaranteed to protect your money.

I believe one of the best ways to help mitigate market risk isn’t by investing in any specific product, but in implementing a strategy called “bucketing.”

What is bucketing?

Bucketing is a method that simplifies financial planning by creating various “buckets” based on your expenses required during certain time horizons.

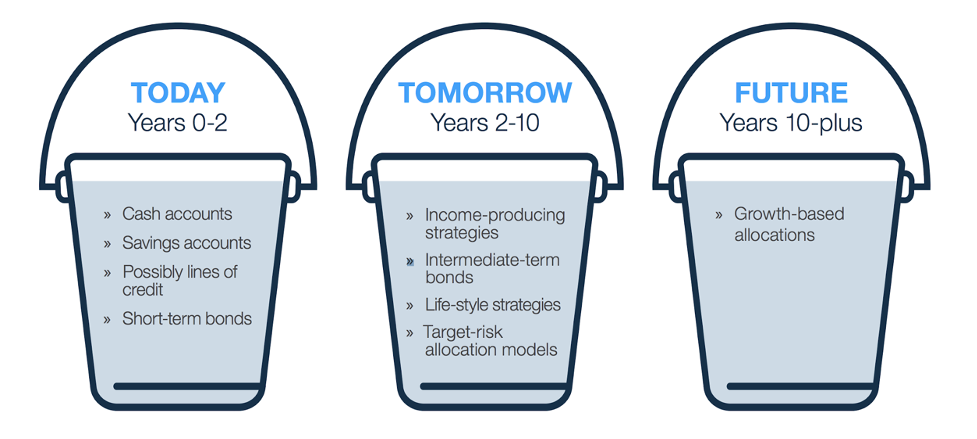

There isn’t a limit as to how many buckets you use, but we recommend using three.

Generally, the simpler your plan, the more clarity and confidence you’ll tend to have.

Our goal in bucketing is for you to have clarity and calm. When you find peace in your plan, you are far less likely to make poor financial decisions based on emotions when the markets are volatile.

Here’s how it looks:

How does bucketing work?

We start by looking at your expenses (your budget) and a list of all of your investment accounts.

All cash, savings, checking and money market accounts get segmented into the first bucket.

First Bucket

The goal of the first bucket is to have enough money in “cash” investments to cover up to two years of expenses. We recommend as little risk on these assets as possible.

This bucket’s purpose is to have available funds for both regular expenses and unexpected emergencies.

Second Bucket

The second bucket includes accounts intended to be spent on major purchases expected in the next two to ten years. This may include college accounts for kids or grandkids, a down payment on a home, lake home, investment property, etc.

You can afford to take on more risk in this bucket because you have more time before you’ll need the money.

We typically have a goal of achieving 4-6% returns on these dollars, depending on how close you are to needing them. When you save intentionally for these medium-term investments now, you are less likely to take on additional debt later. Debt tends to lead to anxiety, and having no debt tends to lead to confidence.

Third Bucket

The third bucket consists of accounts that can provide for our expenses 10 years in the future or more.

The goal is to grow these dollars to the best of our ability. It’s important that you do take on more market risk with these accounts!

We would segregate group retirement plans, IRA’s, pension plans, etc. in this category.

The goal is to maximize long term growth because we all have another risk to consider: the risk we run out of money during retirement.

A 75-year-old retiree has a statistical probability of living longer than ten more years, so they should have a portion of dollars invested in their third bucket as well.

Younger individuals, as long as their first two buckets are in good shape, should be putting the majority of their dollars in the third bucket.

As a person moves towards retirement, we would suggest shifting portions of bucket three into bucket two, and from bucket two to bucket one, until you have up to five years of expenses in bucket one during retirement.

How does bucketing mitigate risk?

The greatest risk to your investments isn’t market volatility. Emotional decision-making poses a far greater threat to return on investment.

When a younger person has two years’ worth of expenses saved in their first bucket, they don’t need to be worried about market volatility because they won’t need to pull the dollars out for at least two years.

The retiree who has five years of expenses covered in cash will probably never have to pull money out of their third bucket during a market downturn – they have time to let those accounts recover.

The decision to separate dollars into buckets based on when you’ll use them leads to peace and allows you to ride any waves the market sends your way.

If you’d like some help creating your own personalized bucket strategy, let’s get in touch and start the conversation.

This piece is not intended to provide specific legal, tax, or other professional advice. For a comprehensive review of your personal situation, always consult with a tax or legal advisor.