Again, the stock market feels like a wild ride, where volatility has become all too normal.

As a financial advisor, I field questions about this frequently, especially during periods like we’ve seen in the first half of 2022.

That said, our team approached me with a handful of questions we hear on a regular basis during volatile times.

I hope you find this useful!

1. What would you tell your anxious friends, family, and clients about the markets?

I typically remind everyone that we’ve been here before and that we need to proceed with a thoughtful and careful approach.

Think about how we parent and protect our children.

What would you do if a kid on the playground hauls off and hits your kid?

My tendency is to allow my strong sense of justice to fuel an overreaction, and it only makes the problem worse. But I’ve learned the hard way that I tend to get better results when I respond thoughtfully, gently and carefully rather than reacting to any situation.

A market downturn can feel like a punch in the face. It’s hard not to panic. But with markets, we need to use self-control and respond with facts and cerebral-based choices and not react with our feelings. As a wise client of mine once stated, “Don’t give your feelings authority in your life.”

Here are some helpful things to focus on during market turbulence and economic uncertainty:

Remember there is nothing new under the sun.

Bear markets/recessions have occurred throughout market history on average every 56 months.

We’ve been through this before… “but did the market come back?”

The simple answer is: yes.

Every rolling 15-year period in market history has had a positive return. In fact, the average recoveries after market downturns are significant!

Remember you are investing for a future harvest.

Imagine planting corn seeds in the Spring.

We then experience an extended drought.

What do you do?

A knee-jerk reaction may be to dig up your seed and try to salvage what you have left for next year. A better response would be to trust that the seed is doing something below the surface even when things feel dry and hopeless. Again, don’t give your feelings authority.

Farmers plant in all conditions and all seasons.

Why is this?

They are planting for a future harvest. They know that most of the seed will grow into a plant that produces 100-fold the old seed.

That’s a good investment. But only if they remain patient and steadfast, trust the seed and the process, and allow it to do what it was made to do.

Don’t dig up your future harvest by cashing in your investments!

Instead, remember what happened historically after market downturns and let the seed do its job through the hard times.

Let your financial plan make your asset allocation decisions. This provides a purpose for your investments.

2. Can you, in simple terms, explain what exactly is happening with the economy?

No.

It’s really complicated, politicized, and hard to determine who is giving facts. Most people have an angle.

I think there are simple fixes, but getting simple things accomplished proves to be very difficult. Understanding the fundamentals of markets and taking a long view of market history is very helpful here. Watching the news is not!

3. How do we prepare our finances for a recession?

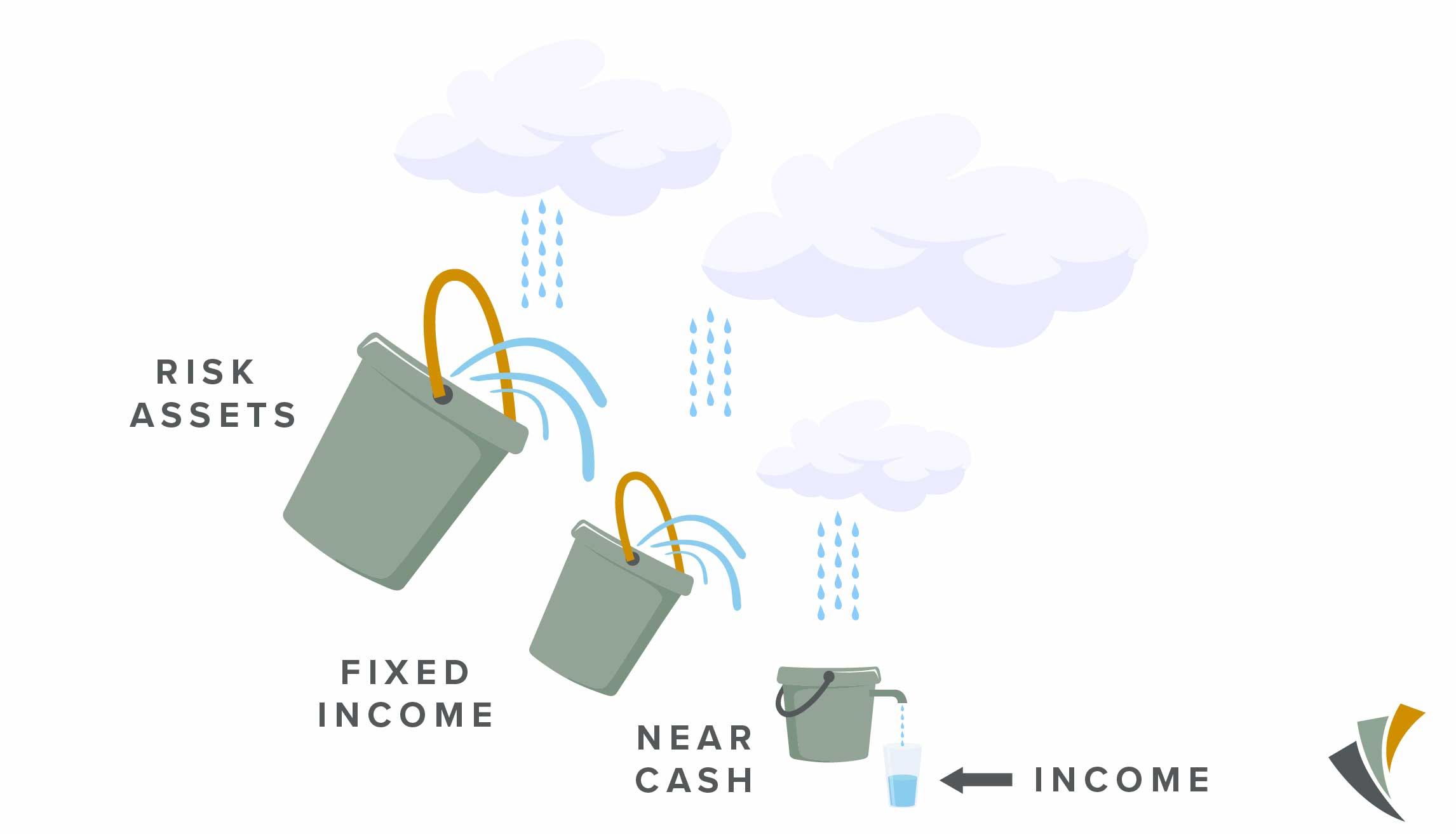

Like insurance, you prepare your finances using the bucket theory BEFORE a bear market, not during it.

Assess your investment fields using the bucket theory. I enjoy this analogy and deploy this strategy daily.

BUCKET 1:

Short-term dollars should be in cash to cover up to two (2) years of non-discretionary expenses. Don’t worry about return on investment OR inflation on these dollars. That’s the job for buckets 2 and 3.

Do not invest these dollars into the market!

BUCKET 2:

Money you’ll need in 2-10 years striving for 4-6% returns.

Focus on steady stocks like utility companies, short to medium-term bonds, I Bonds, etc.

You can let this money ride the market a little longer than the cash, or respond by moving some of these dollars to fill your short-term bucket if a bear market/recession lasts longer than expected.

BUCKET 3:

Long-term dollars go in bucket 3 and aren’t needed for 10-plus years. These are the dollars that go up and down the most as they are invested mainly in growth stocks. When markets go down and your portfolio “loses money,” you should not be surprised. Expect it. Have faith in the process. Let the seed to it’s job.

Remember, this third bucket has time to recover.

If you don’t have 2 years of non-discretionary expenses in cash (what I need to survive) — start saving and setting aside what you can. Give us a call and let’s come up with an efficient plan to make sure this bucket is adequately filled.

4. What should I change with my

financial plan as we potentially enter a bear market?

Markets should not change or guide financial plans.

Your financial plan helps us determine the asset allocation between the buckets. You should be able to weather storms, with possible small navigational shifts to stay on course. This is not a time for overhauling or abrupt shifts.

Stay true to the path set forth in your plan.

I hope these answers are helpful for you as we enter times of volatility.

I assure you this: we have been here before and it is not different this time.

![]()

____________________

This piece is not intended to provide specific legal, tax, or other professional advice. For a comprehensive review of your personal situation, always consult with a tax or legal advisor.

Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns.

Ryan Ovenden is not registered with Cetera Advisor Networks LLC.