By Kevin Engbers

June 3, 2022 —

The philosophy of most investors appears to unite in the desire to have their portfolios move higher, to take advantage of opportunities when they present themselves, and be cognizant of limiting downside movements.

However, there are some fundamental differences when it relates to your life planning targets and the emotions attached to the swings in the markets. This year has all investors revisiting their philosophies as it relates to their financial and life planning targets.

As it relates to investment strategies, this parlays into a topic I want to discuss today, the comparison of two different philosophies — performance-based investing vs. goals-based investing.

At Pinnacle Wealth, we are all-in on goals-based investing.

First, I’ll start with my attempt to define our terms. They are:

- Performance-based investing (PBI): an investment strategy that emphasizes investing with the objective of optimum returns and superior portfolio performance.

- Goals-based investing (GBI): an investment strategy that emphasizes investing with the objective of attaining specific life goals, measuring progress towards those goals, rather than generating the highest possible portfolio return. Learn more here.

Secondly, it’s important to begin with a specific clarification.

This article could easily read like an excuse or justification for poorly performing portfolios. This is not the case whatsoever.

The mindset shift is clearer when you apply the initial definitions of the portfolio returns to your financial and life planning targets. It is the application of the two philosophies that separates the two along with the corresponding emotions anxiety and elation.

The fundamental difference is not about the portfolio, it is about the accomplishment of your life goals.

Look at the difference:

- Performance-Based Planning: your performance will determine your risk, your risk will direct your plan, your plan will dictate your goals which may or may not be your dreams. This is a plan based on optimum returns with less regard for risk and how that affects your life.

- Goals-Based Planning: Your dreams should inspire your goals, your goals should clarify your risk tolerance, your risk tolerance should develop your plan, your plan will dictate your targeted portfolio return expectations.

At Pinnacle Wealth, we are all-in on goals-based investing.

This will all be based on your financial resources and the amount of time until the money needs to present itself to your dream.

At Pinnacle Wealth, we always strive for improving performance and do everything in our power to be fiduciaries for our clients, and that lends itself to the goals-based way.

That said, I write this with an understanding that finances are a part of life, not the focal point of life. It’s an understanding that finances play a key role in True Wealth, but should not be life’s sole objective.

With that in mind, let’s dive in.

The baseball fans reading may enjoy this analogy.

Baseball is a game that functions off of performance and numbers. It’s perhaps the most analytics-driven sport we watch.

Many advisors I watch step to the plate like famed sluggers Reggie Jackson, Alex Rodriguez, Sammy Sosa, or Jim Thome. They dig in and swing for the fences.

When they hit an investment, it works out splendidly. Notice all four of the names listed above are inside baseball’s top-15 in career home runs. People love the long ball.

But what happens when those players don’t hit the ball hard?

All four of the names listed above (Jackson, Rodriguez, Sosa, and Thome) are found inside the top-5 in career strikeouts at the plate. Their career strikeouts outnumbered their career home runs 4:1.

Now the long-ball is attractive. It draws fans and big contracts alike. But the question must be asked:

Is the point of baseball to hit the ball the furthest, or is it to score the most runs?

Let’s look at the all-time runs leaders.

From our example above, only Rodriguez above can be found inside the top-10 in career runs scored (he’s 8th). The other three cannot be found inside the top-50.

The all-time leading run scorers were players like Rickey Henderson, Ty Cobb, and Barry Bonds — players who possessed discipline to get on-base.

They got on-base early — and often.

By getting on-base, they optimized their opportunity to score. In turn, they increased their team’s chances of winning the game.

At Pinnacle Wealth, we still want to hit for power. After all, Bonds did both. But at the same time, we also swing with a specific intentional discipline to get on base.

After all, it’s about scoring runs. You score runs by getting on-base and optimizing for success.

That’s how you win the game.

Does that analogy land home?

I would say among the most common questions we receive as advisors revolve around two objectives: performance and fees.

Our team agrees — investment management is critical. I don’t want to discount that. Our team, as a Carson Partner, works tirelessly to serve our clients and steward their assets.

Although we are often asked about performance and fees, we’re rarely asked about goals.

Because it matters not as much “what” is in the car, but “where” is the car going?

Where investment management is critical, investor management is perhaps equally, or moreso, important.

Ask yourself these key questions:

- What do I need my money to do to achieve contentment now and in the future?

- When is the best time for me to know what I need for my retirement?

- What goals am I optimizing for?

There are two key distinctions between performance-based investing and goals-based investing.

Performance-based is a default formula.

It’s an idea that whatever happens, happens. It’s a “let the thing grow, and that’s where I’ll be, I guess,” approach.

If you can assure with certainty premium returns, it can win. But there’s not much design.

It’s blazing across the lake in a speed boat at full speed, hoping that you know where you’re going and that you won’t hit anything along the way.

Goals-based is a designed formula.

Understanding goals-based is about blueprinting your life, seeking to realize the goals you have set before you.

It requires thought, strategy, specific goals, along with an understanding of where you’re going. You’re managing to reach your goal instead of chasing outcomes.

It’s a life by design.

If an 8 or 9% return will help you achieve your goals, why pursue 12% if it could be easily derailed with unneeded risk?

Now before I wrap-up this blog, you’re probably asking yourself the basic fundamentals of goals-based investing.

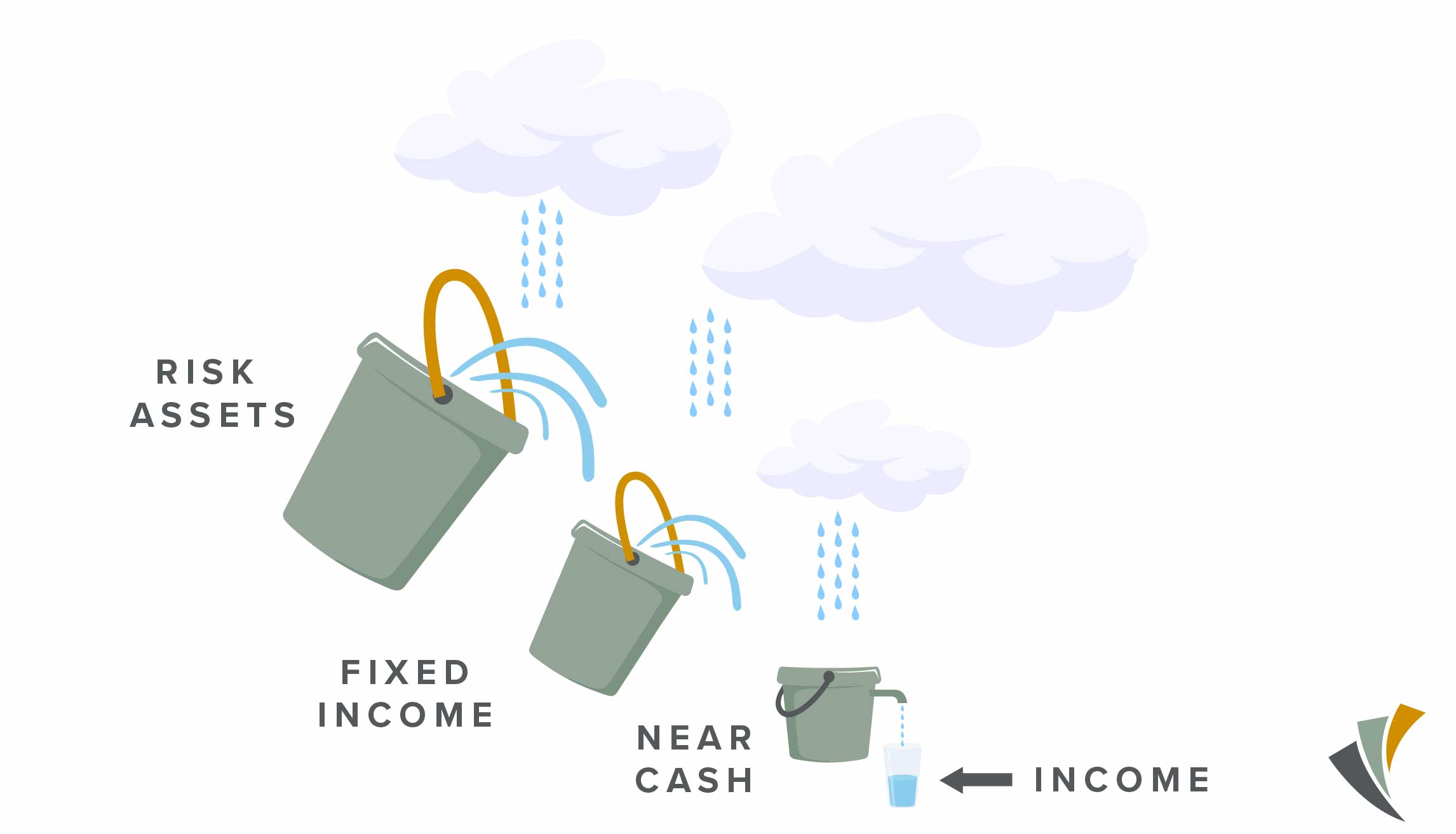

One of my favorite philosophies is that of “bucketing.”

This could easily be an entirely different blog post or video, but imagine you have three buckets. Each of these buckets will hold a certain amount of your portfolio.

- Bucket one (1-2+ years) has two years of income sitting there for you. It’s there to provide you with an income stream. It might be held in a combination of low-risk investments, a mix of cash, short-term bonds, CDs, and simple money markets. It’s serving a specific purpose — to provide you with stable income and access for liquidity.

- Bucket two (3-5+ years) will be placed in fixed incomes and will be a broadly-based portfolio. It will be vested, but mostly conservatively. It’s an earner.

- Bucket three (10+ years) will need to grow in order to refill both buckets one and two. Bucket three will be primarily in securities, gaining exposure to an array of growth potential. Bucket three is the true grower.

Now if you’re a younger investor, you may hold 80% or more of your portfolio in bucket three. This investor has a higher risk tolerance given their age.

They may have less than 5% in bucket one.

Older investors may see a much different makeup. They may have 30% in bucket one, another 35-40% in bucket two. They are working to mitigate their risks.

All of these allocations would be built around goals.

Yes, that’s goals-based investing.

Volatility is still expected. You cannot avoid it. Both strategies can experience downturns and negatives. That’s the nature of investing.

But these downturns only become detrimental when one loses sight of their goals.

Before our team works with anyone, we ask them a key question: why do you want to build wealth?

We ask them the same three questions I mentioned earlier.

- What do I need my money to do to achieve contentment in the future?

- When is the best time for me to know what I need for my retirement?

- What goals am I optimizing for?

Responsibility is about contentment. It’s not investing to chase returns or seek prodigious wealth.

In my experience, people are never satisfied when seeking ‘more, more, and more.’

They may find themselves financially wealthy, but spiritually, emotionally, and physically broke.

A great legacy isn’t built when you die. It’s built with the way you live.

Let’s build your plan to pursue that legacy.

All investing involves risk, including the possible loss of principal. There is no assurance that any investment strategy will be successful.