2021 was a very happy year for U.S. stock investors. The S&P 500 finished the second year of a pandemic 28.7% higher than it started the year. Other countries did not do as well. The MSCI ACWI, which includes U.S. stocks, rose 18.5% in 2021. Those returns are still very impressive, but they lag behind the S&P 500. Bonds declined slightly. The Bloomberg U.S. Aggregate Bond Index slipped 1.5% last year.

Key Points for the Week

- The S&P 500 returned 28.7% in 2021 as large U.S. companies continued to outperform many asset classes.

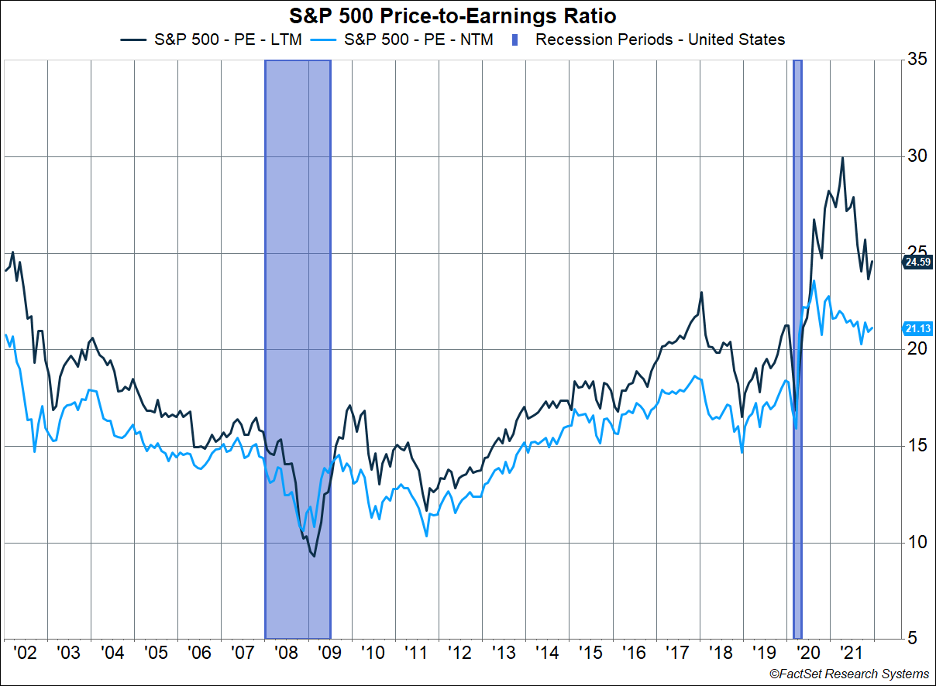

- Valuations on the S&P 500 remain above average even though strong earnings have helped reduce ever higher valuations from late last year.

- Industrial production data from Japan and South Korea show those two countries are helping to ease the shortage of semiconductors and automobiles.

Earnings are likely to have grown more than 45% in 2021, based on the first three quarters of results and estimates for the fourth quarter. As shown in Figure 1, the strong earnings growth allowed the price-to-earnings (P/E) ratio to drop in 2021 even though markets moved significantly higher. While valuations have declined, they remain above average and are being supported by low bond rates. Figure 1 shows the next 12-month earnings (NTM) have fallen from a peak of 30 to just under 25. The last 12 months (LTM) P/E ratio has also declined.

Moving back to fundamentals, industrial powerhouses Japan and South Korea reported strong bounces back in industrial production after having slowed in October. Strength in auto and semiconductor manufacturing boosted Japan to 7.2% growth and South Korea to 5.1% growth.

Weekly results were in line with the yearly themes. The S&P 500 index added 0.9% last week. The MSCI ACWI gained 0.8%. The Bloomberg U.S. Aggregate Bond Index added 0.2%. The U.S. employment report will headline a series of key labor market reports this week.

Figure 1

Three Big Shifts in 2021

Why do people set New Year’s resolutions? Humans use auspicious dates, such as New Year’s or birthdays, to evaluate their lives and plan for next steps. Nothing stops us from setting our next big goals on August 10, but those with birthdays on that day are much more likely to do so than the rest of us.

The downside of this approach is we start to lump time periods together based on the calendar and attribute more meaning to those periods than they deserve. A natural consequence is failing to notice major changes because the annual data obscure some underlying movement.

In this week’s update, we review three keys shifts from 2021 that will likely shape markets in the coming year.

Interest Rates

The biggest shift occurred in interest rate policy. The supply shortages and government stimulus proved too much for supply structures, and the Fed turned hawkish as inflation rose. The first step was to begin reducing extra purchases of government bonds and mortgages. Once those extra purchases have tapered to zero, the Fed signaled it will likely move rates away from the near 0% rate it established shortly after the pandemic began.

Chinese Policy

China shifted away from a free-market approach for its most innovative companies and moved toward reining them in with more regulation. Those companies had made their founders and others very wealthy. But rather than embrace that growth, President Xi Jinping sought to reshape it with an emphasis on a broader distribution of wealth. The resultant risk for Chinese companies is one reason emerging markets finished lower last year.

Sector Performance

Another example of the calendar giving the wrong impression comes from style box performance. “Small value” was the top performing style box in the Morningstar Style Box universe, rising 31.8% last year and beating out second place “large core,” which rose 29.3%. It would be logical to assume small-cap value had some momentum going into 2022. But the truth is small-cap value built up a big lead and then limped to the finish. In the first five months of the year, small value gained 31.5% and outperformed large core by more than 20%. For the last seven months small value barely moved while large core posted steady gains.

2021 will go down for most of us as the second year of the COVID-19 pandemic. As we enter the third year of wrestling with the virus, our focus will rightly be on managing life. Yet, some major shifts are occurring that may turn out to be very important next year, especially if COVID begins to fade.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

Morningstar U.S. Small Cap Value

The index provides a comprehensive depiction of the performance and fundamental characteristics of the Small Value segment of U.S. equity markets. This Index does not incorporate Environmental, Social, or Governance (ESG) criteria.

Morningstar U.S. Large Core

The index measures the performance of US large-cap stocks where neither growth nor value characteristics predominate. This Index does not incorporate Environmental, Social, or Governance (ESG) criteria.

Compliance Case #01230023