It’s among the most popular resolutions that Americans face — especially this time of year.

In November of 2020, Statista surveyed 542 U.S. adults and found that 30% listed “live more economically” on their list of Top New Year’s Resolutions for 2021. It ranked 5th on the list for most popular resolutions.

Translation: “I want to get on a budget.”

People know that managing their resources is critical to living a healthy, balanced life.

We believe it’s critical toward achieving True Wealth, the Pinnacle Wealth way.

Our Philosophy: A Cash Flow Management Plan

Naturally, our team at Pinnacle Wealth has grown accustomed to questions surrounding this topic over the years. We’ve worked with hundreds of couples and individuals through this exercise of telling their money where to go.

That said, I have a very important disclaimer before I start talking about ‘budgets.’

I absolutely hate the word ‘budget’ with a passion.

I much prefer using the phrase “Cash Flow Management Plan.”

I see ‘budget’ as akin to ‘dieting.’

People don’t stick to diets. They stick to healthy lifestyles that have a plan.

I’ve learned the same is true for budgets. People simply don’t stick to them. Instead, they stick to Cash Flow Management Plans.

The question to ask yourself is, “if I have cash coming into my life, how am I managing its flow in and out of my accounts?”

A budget — similar to a diet — also has a restrictive tone. I don’t believe we should be living constrained lives.

Guilt is a poor teacher.

No more nickel and diming our lives, rather let’s establish a game plan for our big chunks of money and work to instill tracking methods for those habits.

It may seem insignificant, but I will not be using the word ‘budget’ for the remainder of this blog, but I digress.

Building a plan is critical, and it’s Biblical.

See Luke 14: 28-30:

“Suppose one of you wants to build a tower. Won’t you first sit down and estimate the cost to see if you have enough money to complete it? For if you lay the foundation and are not able to finish it, everyone who sees it will ridicule you, saying, ‘This person began to build and wasn’t able to finish.”

Let’s develop a strategic plan and manage our money well — on purpose.

“I absolutely hate the word ‘budget’ with a passion.”

– Kevin Engbers

I much prefer using the phrase Cash Flow Management Plan.”

The First Step

The most common first step I see toward building a Cash Flow Management Plan is immediately opening up a spreadsheet, or loose sleeve of paper and start aimlessly filling numbers.

I would not encourage you to make that your first step.

To move forward, we must first look back.

Your first step should be to establish where your money has gone over the past 60-90 days. We’ve always found 90-days (3 months) to be a good barometer.

Before we can move forward with a plan, we need to understand where our money has gone.

Every NFL team does this. Before looking ahead to an opponent for the following week’s game, they look at the film of themselves in the week prior. Review is the first thing they do.

We need to do the same — let’s look at the tape.

Export all of your spending reports (bank statements, credit card statements, etc.) for the previous three months.

Then, try to find a way to estimate cash spent, though I know it’s hard. And if you frequently use other payment methods (PayPal, Venmo, etc.), check those, as well and export.

Then, cluster your spending into the following simple categories:

- All Housing expenses

- Food

- Clothing

- Transportation

- Entertainment

- Medical

- Insurance

- Children

- Gifts

- Miscellaneous

- Margin (saving + investing)

Once you have your three-month averages, we can start to make our evaluation.

Key Rules of Thumb

Everyone finds it easier to play the game once they know the rules.

Looking at your previous three-months with no frame for reference can be daunting, there’s no doubt about it.

We always feel it’s best to break things down into percentages of income. Everyone’s income is different and circumstances can vary.

Having simple rules of thumb for your cash flow management gives you a framework to work within during your evaluation process.

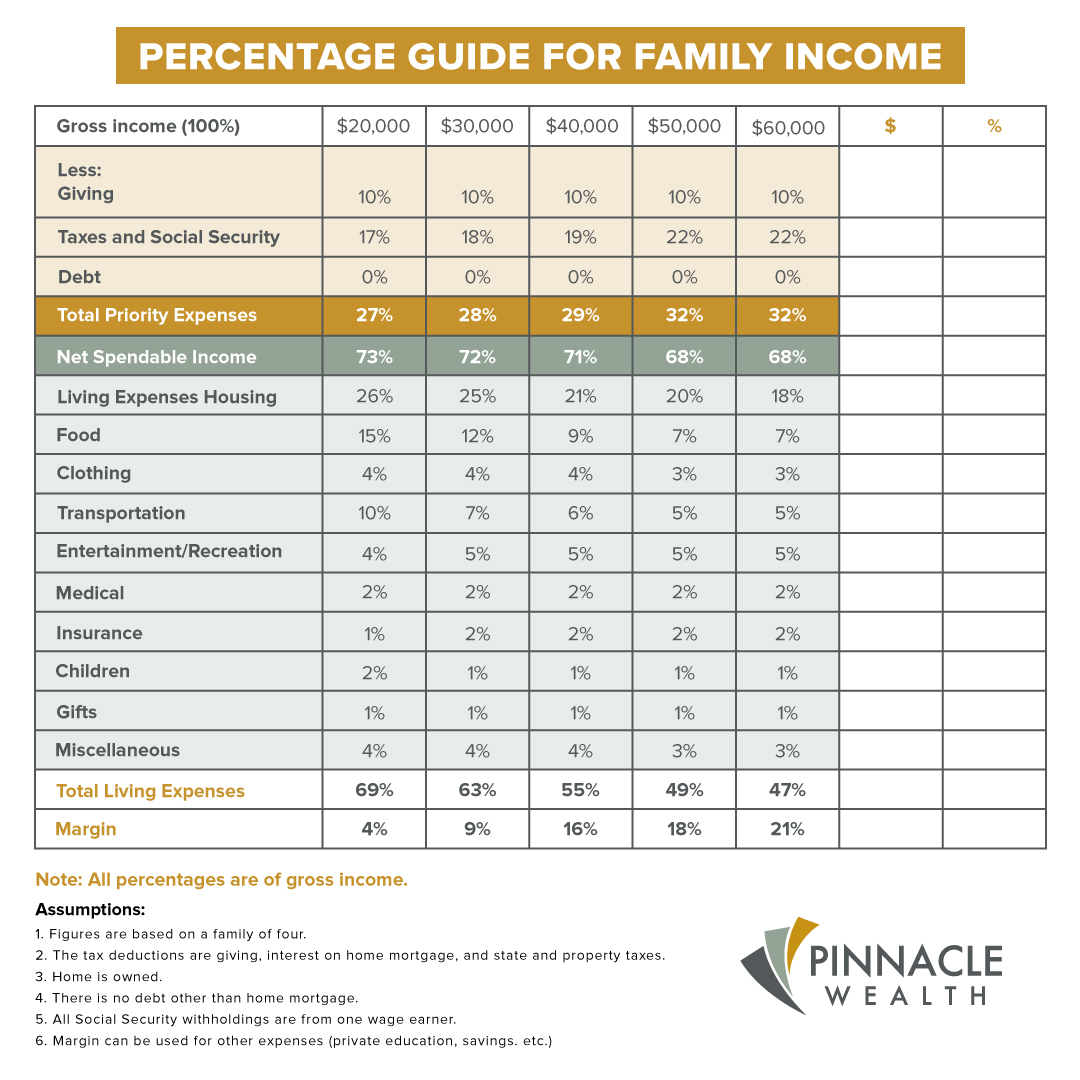

Below is a sheet that outlines folks with income ranging from $20,000 – $60,000 annually. If you earn more than that, which I suppose some of you do, apply the percentages similarly.

Before matching up your cash flow with the chart above, I’d like for you to fill in your three-month averages along each line item.

Then, divide by your income.

Notice anything out of whack?

Let’s make those adjustments when we build out our Cash Flow Management plan for your life.

A Few Helpful Tools

When I got into the industry, the classic budgeting tool was a pen and pad. I don’t mean to date myself with that, but it’s true.

However, there are a number of tools available to set up a plan that works for you.

A major thing I’ve noticed: the tools we use to build our Cash Flow Management plans are largely dependent on generations.

I see younger folks (age 18 to low 30s) using a lot of technology. They easily acclimate themselves to new and ever-adapting applications and software tools. A few that I’ve really liked working with are Mint and Every Dollar.

But there are many sufficient softwares, so do the research yourself.

Middle aged friends of mine (age 40s – 50s) tend to be a bit of a mixture. Many of them will use traditional spreadsheets that they’ve built for their family, along with some usage of the latest apps.

Older folks (age 60s and plus) will still sometimes be rocking life with the pen and pad, and many of them are killing it with their money management!

That’s not to say there aren’t a few of my savvy older client relationships that know their way around a mean spreadsheet, too.

It’s a personal thing and do what works for you.

The simplest method for managing your cash flow is still the envelope system.

If you’re familiar, I need not say more. If you’re not, Dave Ramsey has been explaining it easily for years. If your finances are messy, I would strongly recommend starting here for a few months. It helps immensely.

I love suggesting that people also read Total Money Makeover by Dave Ramsey. He has a phenomenal heart for teaching this content.

So, select the option that works best for you:

- Spreadsheet

- Mint

- Every Dollar

- Pen and Pad

- Envelope System

And let’s get started with planning.

Building Your Cash Flow Management Plan

When it’s time to build your plan, I prefer teaching people to look at the ‘chunks’ of their spending, instead of the ‘morsels.’

Instead of going line-by-line, look at the aggregate of your spending by category. That’s where your 90-days of research comes in handy. Adjust in the areas that you’re overspending and maintain commitment to the areas where you’re already doing well in.

If you notice that you’re not giving, incorporate that into your cash flow plan. At Pinnacle Wealth, we believe that giving opens your finances to blessing, starting by the way you perceive your money.

Let’s go item-by-item and provide definitions and insights.

Here is the chart, as a reminder:

Gross income:

This should be the aggregate total of all of your pay from all primary jobs, side hustles, and more. This is a singular number that comes in every month. If your income fluctuates, average it.

Giving:

We believe that giving is instrumental in understanding your finances.

Taxes and Social Security:

Thankfully for many, employers handle this messy work. If you’re self-employed, it’s on you.

Debt:

This number will vary depending on situation. We encourage you to put all of your margin dollars to your debt. We would also encourage you to cut as many other costs as possible and allocate that to debt until all debt (outside of your mortgage) is paid off.

Housing:

This adds up rent, mortgage, interest, taxes, utilities, and other housing expenses.

Food:

Eating out or eating in, this is all food.

Clothing:

We allocate for clothing, but if you’re in debt, you should consider allocating this payment to your debt and trust that the clothes you presently own are probably sufficient for now.

Transportation:

Cars, insurance, gas, and other transportation costs are included here.

Entertainment:

To make life fun, you need to have money for entertainment. But let’s make a plan for it, so we have the freedom to spend.

Medical:

Every family has a different situation here, so we’d encourage you to evaluate with wise counsel.

Insurance:

These are miscellaneous insurances that do not fall under home and car. Insurance should be used as a way to prevent financial calamities, so approach with caution.

Children:

Other costs for your kids, depending on family size.

Gifts:

Different from your giving fund, this is where birthdays and Christmases are allocated.

Miscellaneous:

We would prefer you find a line item to allocate every dollar. No dollar is truly miscellaneous. If it’s consistent spending, plan for it.

Margin:

This is your margin of money that should, at a minimum, be poured into your savings and investments. We believe your savings should have 6mos worth of living expenses in reserves to serve as an Emergency Fund. To break it down further, 2-months’ worth should be in high-liquidity investments (cash or savings) and the remaining 4-months placed in low-interest, fixed-income safety nets. We touch on this in a different blog.

Now your plan is well on its way. The exercise of preparing a cash flow plan is more important than strictly following it to the dollar each month.

As for sticking to it…

Accountability

The best rules are the simplest; spend less than you make.

People tend to make it more complicated than it needs to be. Once you have your plan, compare your plan to your actual spending.

Your review process should be dependent on the nature of your situation.

If your finances are a disaster, review this weekly. Otherwise, most people should do this either monthly or quarterly.

Monthly is great for most.

While we believe that commitment to your cash flow management plan is important, do not treat it as though it is law. It’s a formula for creating long-term habits. Those long-term habits help you achieve your long-term goals. In reality, it’s nothing more than that.

I remember when times were tough for my wife and I. When money was tight, I would carry around a notebook and I would write down each of my expenses. If I bought a hot dog at the gas station, it made its way into the notebook.

My wife and I made a rule that I wasn’t allowed to go into Best Buy alone. Technology is a weak spot for me. We still have this rule in place at our house, many years after I stopped using the notebook.

At the end of the day, it’s about creating systems that allow for stewardship of your income.

Our team at Pinnacle Wealth absolutely loves serving in this capacity, so if you’re in need of a third-party, consult our team. We would love to help.

Conclusion

Remember, there are tools at your disposal to accomplish the financial goals you’ve set for yourself. We’re willing to help you implement them.

We hope this promotes unity and freedom in your life and allows you to spot problems before they happen. All the while, you’re able to start to prepare for the unexpected and the future.

We’re eating our vegetables and exercising here.

That’s not a diet, that’s a healthy lifestyle.

Good luck with your Cash Flow Management Plan.

Contact anyone on our team with your questions.